Pro Actively Downsizing

Creative solutions for retirees

Jack and Lisa Smith, a couple in their mid-sixties residing in their beloved family home valued at $2.5 million, found themselves facing a substantial financial dilemma. They were experiencing a monthly shortfall of $2,500, which was causing concern, and they also needed $25,000 for an unexpected roof replacement. Although the Smiths were adamant about not wanting to downsize due to the countless memories they had created with family and friends in their cherished home, their financial situation prompted them to consider two alternatives:

Option 1 - Using investments: The Smiths considered withdrawing $2,500 monthly and taking a one-time $25,000 withdrawal for roof repair. However, this would deplete their investments sometime between the ages of 72 and 77.

Option 2 - Turn to Children for support: The Smiths thought about asking each of their children for $1,250 per month or a one-time $12,500 each for the roof repair. But they hesitated, knowing their children's financial situations weren't ideal for ongoing support. Both options seemed uncomfortable, and the Smiths wished to maintain their independence and not burden their children

Solution: Seeking an alternative to downsizing and selling their family home, they explored Reverse Mortgages options. This allowed them to access their home's equity without selling, providing a reliable source of income. While there are many ways that a reverse mortgage can help provide income for the Smiths, they were particularly attracted to a strategy called proactive downsizing.

Proactive Downsizing

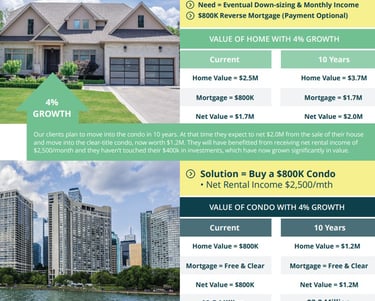

Our clients have a free & clear primary residence but are planning ahead for when they will sell and move to a condo. They also need a supplement to their monthly income and would prefer not to start drawing on their investments.

Get in

touch.

604-353-9254

martine@arcmortgage.ca

Team - Arc Mortgage LTD

BRX - Arc Mortgage