Why isn’t reverse mortgage money taxable?

A reverse mortgage is a loan secured against your home, not income from employment, investments, or government benefits. The Canada Revenue Agency (CRA) only taxes income—not borrowed money.

Why isn’t reverse mortgage money taxable?

A reverse mortgage is a loan secured against your home, not income from employment, investments, or government benefits. The Canada Revenue Agency (CRA) only taxes income—not borrowed money.

Here’s why it’s tax-free:

You’re not earning money, you’re accessing your home equity

The funds are considered loan proceeds, not income

You’re not required to make monthly payments, but interest accrues over time

Repayment happens later—usually when the home is sold

Because of this structure, reverse mortgage funds don’t show up on your tax return.

Does a reverse mortgage affect government benefits?

One of the biggest concerns I hear is whether accessing home equity will reduce benefits like OAS or GIS.

Good news:

OAS (Old Age Security): Not affected

CPP (Canada Pension Plan): Not affected

GIS (Guaranteed Income Supplement): Not affected

Since reverse mortgage funds are not classified as income, they don’t trigger clawbacks or reductions in these programs.

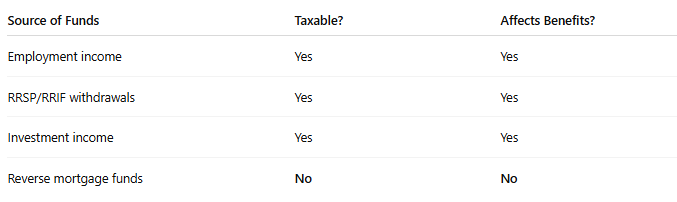

How is this different from other retirement income?

Here’s a simple comparison to clarify:

This makes reverse mortgages a powerful option for retirees who want to access cash without increasing their taxable income.

When might taxes still come into play?

While the reverse mortgage itself is tax-free, there are a few indirect scenarios to keep in mind:

1. Investing the money

If you invest the funds you receive and earn interest, dividends, or capital gains:

That investment income is taxable

2. Rental or business use of your home

If your home is partially used to generate income:

There may be tax implications when the property is eventually sold

3. Estate considerations

When the home is sold to repay the loan:

There is usually no tax on your principal residence (thanks to the principal residence exemption in Canada)

Real-world example (Canada)

Let’s say you’re a homeowner in Ontario:

Your home is worth $800,000

You take a reverse mortgage for $200,000

You receive the money in monthly payments

That $200,000:

Is not taxed

Does not reduce your OAS or CPP

Can be used freely—for living expenses, travel, or helping family

If you invest part of it and earn returns, only those earnings would be taxed.

Common mistakes to avoid

Assuming it counts as income: It doesn’t—this is the biggest misconception

Forgetting about interest accumulation: While not taxable, the loan balance grows over time

Investing without tax planning: Returns on invested funds are taxable

Not reviewing your full financial picture: A reverse mortgage works best as part of a broader retirement strategy

Who is a reverse mortgage best for?

A reverse mortgage can be a strong fit if you:

Are 55 or older

Own a home in Canada

Want to access tax-free cash flow without selling

Prefer to avoid increasing taxable income

Want to stay in your home while improving financial flexibility

Should you talk to a mortgage expert?

Every situation is different. While reverse mortgages offer clear tax advantages, it’s important to understand how they fit into your full financial plan.

As a mortgage broker specializing in reverse mortgages, I help Canadians:

Understand exactly how much they can access

Structure withdrawals in the most tax-efficient way

Avoid common pitfalls

If you’re considering this option, a quick conversation can bring a lot of clarity.

Frequently Asked Questions

Is a reverse mortgage considered income in Canada?

No. It is considered a loan, not income, so it is not taxed.

Do I need to report reverse mortgage money on my tax return?

No, you do not report it because it is not taxable income.

Will a reverse mortgage affect my OAS or CPP payments?

No. These benefits are not impacted because reverse mortgage funds are not income.

Is there any situation where I would pay tax on a reverse mortgage?

Not on the loan itself—but if you invest the funds and earn income, that income is taxable.

What happens tax-wise when my home is sold?

If it’s your principal residence, it is generally exempt from capital gains tax in Canada.

Can I use reverse mortgage money however I want?

Yes. There are no restrictions—you can use it for living expenses, home improvements, or anything else.

Is a reverse mortgage better than withdrawing from my RRSP?

It depends. RRSP withdrawals are taxable, while reverse mortgage funds are not. The right choice depends on your financial situation.

About the Author

Martine Perron is a Canadian mortgage broker specializing in reverse mortgages. She helps homeowners aged 55+ access their home equity safely and strategically.

👉 Book a consultation: https://app.arcmortgage.ca/widget/bookings/private-consultation-with-martine-perron

Get in

touch.

604-353-9254

martine@arcmortgage.ca

Team - Arc Mortgage LTD

BRX - Arc Mortgage