Do You Have to Downsize to Access Money in Retirement?

No—you have options beyond selling your home. While downsizing can free up cash, it also comes with costs, stress, and lifestyle changes that many retirees want to avoid. According to the Canada Mortgage and Housing Corporation (CMHC), most Canadian seniors prefer to age in place, meaning they want to stay in their current home as long as possible. This is especially true in high-cost markets like Vancouver, where moving may not significantly reduce expenses.

Watch: Downsizing vs Using Home Equity in Canada

If you're wondering whether you really need to move, this short video explains your options clearly:

What Does Downsizing Actually Mean?

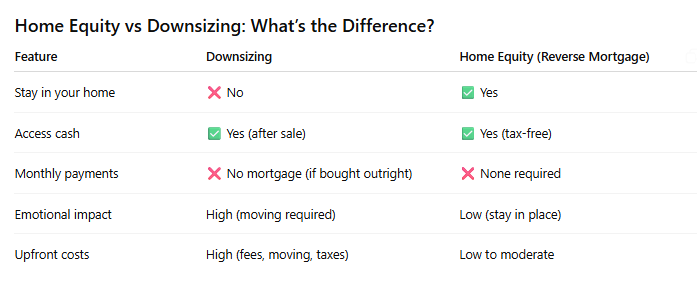

Downsizing means selling your current home and buying a smaller, less expensive one. The difference in price becomes available cash you can use in retirement.

Pros of Downsizing

Access to a lump sum of cash

Potentially lower monthly housing costs

Opportunity to simplify your lifestyle

Cons of Downsizing

Realtor fees, legal costs, and moving expenses

Emotional impact of leaving your home

Limited affordable options in cities like Vancouver

Disruption to your community and routine

Source: CMHC highlights that both financial and emotional factors often make downsizing less appealing than expected.

What Are the Alternatives to Downsizing in Canada?

If your goal is to access money without moving, here are the main options:

1. Reverse Mortgage

A reverse mortgage allows homeowners aged 55+ to borrow against their home’s value without selling.

Receive tax-free cash

No required monthly payments

Stay in your home

Source: Financial Consumer Agency of Canada (FCAC) confirms reverse mortgage funds are not considered taxable income.

2. Home Equity Line of Credit (HELOC)

Requires income qualification

Requires monthly payments

Variable interest rates

Source: notes that HELOCs may be harder to maintain on a fixed retirement income.

3. Mortgage Refinancing

Requires income and credit qualification

May increase monthly payments

Subject to federal stress test rules (OSFI)

Home Equity vs Downsizing: What’s the Difference?

When Does Downsizing Make Sense?

Downsizing may be a good fit if:

Your home no longer meets your needs

You want a lifestyle change

You’re comfortable moving

You find a significantly cheaper home

However, in Vancouver, many homeowners are surprised to find that downsizing doesn’t free up as much cash as expected after costs.

When Is Accessing Home Equity a Better Option?

Staying in your home may be the better choice if:

You want to age in place

You value your current neighborhood

You need additional income or flexibility

You want to avoid the stress of moving

A Real-World Example in Canada

Let’s say you own a home in Vancouver worth $1.5 million.

Downsizing: After buying a smaller home and paying fees, you may net ~$300K–$350K

Reverse mortgage: You could access up to 55% of your home’s value depending on your age—without moving

This is why many retirees explore home equity first before deciding to sell.

Common Mistakes to Avoid

Assuming downsizing is your only option

Underestimating transaction and moving costs

Ignoring emotional and lifestyle factors

Not exploring all available financial solutions

Who Is This Best For?

This is especially relevant if you:

Are 55+ and own your home

Live in a high-value market like Vancouver

Want to increase retirement income

Prefer to stay in your home

Final Thoughts from Martine Perron

You may not need to move after all. Many Canadians are surprised to learn they can unlock the value of their home without selling it.

Downsizing is one option—but it’s not the only one, and it’s not always the best one.

If you’d like help comparing your options based on your situation, I’m here to guide you through it clearly and confidently.

Frequently Asked Questions

1. Do I have to sell my home to access equity?

No. Options like reverse mortgages allow you to access equity without selling.

2. Do most Canadian seniors downsize?

No. CMHC reports that many prefer to stay in their homes and age in place.

3. Is reverse mortgage money taxable?

No. It is tax-free.

4. What is the biggest downside of downsizing?

Costs, stress, and the emotional impact of moving.

5. Can I stay in my home and still get extra income?

Yes. Home equity solutions are designed for that.

6. Is this common in Canada?

Yes—especially in expensive housing markets.

7. How do I know which option is right for me?

It depends on your goals, finances, and lifestyle—this is where personalized advice helps.

Sources

Canada Mortgage and Housing Corporation (CMHC) – Aging in place and senior housing trends

Financial Consumer Agency of Canada (FCAC) – Reverse mortgages and home equity borrowing

Office of the Superintendent of Financial Institutions (OSFI) – Mortgage lending guidelines

About the Author

Martine Perron is a Canadian mortgage broker specializing in reverse mortgages. She helps homeowners 55+ access their home equity without giving up the home they love.

👉 Book a personalized consultation here: https://app.arcmortgage.ca/widget/booking/3XlppqW68zlsLr2daWK3

Youtube video: https://youtube.com/shorts/6dZEdsS2oAE?si=QWFv4T_gaJ5qQrZ1

Get in

touch.

604-353-9254

martine@arcmortgage.ca

Team - Arc Mortgage LTD

BRX - Arc Mortgage